AQA AS Economics Questions With Answers

- AQA AS Economics Unit 1 Section A

- AQA AS Economics Unit 1 Section B Part 1

- AQA AS Economics Unit 1 Section B Part 2

- AQA AS Economics Unit 2 Section A

- AQA AS Economics Unit 2 Section B part 1

- AQA AS Economics Unit 2 Section B part 2

- AQA AS Economics 2015 Unit 1 Section A

- AQA AS Economics 2015 Unit 1 Section B Part 1

- AQA AS Economics 2015 Unit 1 Section B Part 2

- AQA AS Economics 2015 GCSE solved Question Paper

Section A: Objective Test

Q.1. A production possibility frontier illustrates

- the various combinations of output an economy will produce with its limited resources.

- the various combinations of output an economy is currently capable of producing with its limited resources.

- the maximum output an economy will ever be capable of producing.

- the various combinations of output which can be produced at zero opportunity cost to society.

ANSWER- option(b)

A production possibility frontier refers to the graphical representation of the various combinations of two goods which an economy can produce given the availability of necessary resources and technology. PPF represents alternative production possibilities of two goods open to an economy in the current availability of limited resources and technology.

Q.2. Which one of the following would be classified by an economist as an example of the factor of production known as capital?

- A delivery van

- Stocks and shares

- Savings in the bank

- Underground reserves of coal

ANSWER-option (a)

Delivery van will be classified as a capital. Capital refers to anything produced to be used further in production of goods and services. A delivery van is a capital good produced to increase the productive capacity of a business by providing distribution (of raw materials or finished goods) services.

Q.3. Which one of the following combinations, A, B, C or D, correctly identifies the operation of both the rationing and incentive functions of the price mechanism?

| Price change | Rationing function | Incentive function | |

|---|---|---|---|

| A | Rise | More supplied | Less demanded |

| B | Fall | More supplied | More demanded |

| C | Rise | Less demanded | More supplied |

| D | Fall | More demanded | More supplied |

ANSWER-OPTION (C)

The interaction of buyers (demanders) and sellers (suppliers) in a free market help in efficient allocation of resources.

Whenever there is scarcity of a good (or say resource), then demand exceeds the supply of that good. This drives the price up in order to discourage demand. In other words, greater the scarcity (demand>supply), higher the price and thus more resources are rationed (contraction of demand by higher price). Higher price provide incentive to the producers (or sellers) to supply because of increased profitability. Thus, we infer the following result:

PRICE RISE— LESS GOOD DEMANDED (rationing function) ̶MORE SUPPLIED (incentive function).

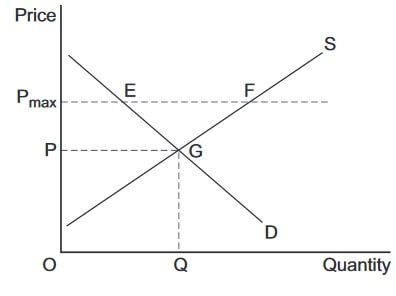

Q.4. The diagram below shows the supply of, and demand for, milk with the initial price at OP. A government now decides to impose a maximum price of Pmax.

The most likely outcome would be

- excess supply of milk at EF.

- a shortage of milk at EF.

- the equilibrium price OP being maintained.

- a reduction in price from Pmax to OP.

ANSWER-OPTION (C)

The equilibrium price of OP will be maintained. Here, we have a situation of Price ceiling. Price ceiling refers to the maximum price that is imposed by the government at a level lower than the equilibrium price (OP).Here, the price ceiling is not binding as the maximum price fixed is above the equilibrium price. The price ceiling above the price level realized by the market has no effect as the market will equate supply and demand and thus equilibrium price will be maintained.

Q.5. The demand for capital goods such as plant and machinery is said to be an example of derived demand because the demand for capital goods depends on

- the productivity of capital goods

- the volume of consumer goods purchased.

- the price of capital goods.

- the amount of labour employed by a firm.

ANSWER- OPTION (B)

The demand for capital good is a derived demand. It is determined by the volume of final consumer goods sold. The demand for capital good is directly related to the demand for the final good. If the demand for final good rises then the amount of plant and machinery required to produce that good also rises.

Q.6. Which one of the following is the most likely reason for government intervention in a market to correct a misallocation of resources?

- A low price elasticity of supply of a good

- Immobility of factors of production

- Diseconomies of scale in production of a good

- An excess market demand for a good

ANSWER – OPTION (B)

Factor immobility occurs when it is difficult for the factors of production to move between different expanse of the economy. There are two types of market factor immobility, occupational immobility and graphical immobility.

Occupational immobility occurs when there are barriers to the movement of factors of production (labor and capital) between different sectors of the economy. This leads to these factors remaining unused or unemployed. People experience occupational immobility because of a mismatch between the skill that an unemployed has and the skill that the employer is looking for.

Geographical immobility refers to a situation resources especially labor do not freely move from one location to another. This refers to the barriers that prevent people from moving from one place to other to find work.

Government can improve or make changes in the country’s education system by introducing new Assignments (or remolding existing ones) that cater to the needs of the economy

Q.7. The table below shows changes in labour productivity for a firm over time.

| Year | Index of labour productivity (2010 = 100) |

|---|---|

| 2008 | 110 |

| 2009 | 103 |

| 2010 | 100 |

| 2011 | 102 |

| 2012 | 111 |

The data show that over the period 2008 to 2012

- the total output of all workers was highest in 2012.

- productivity changed at its fastest rate between 2008 and 2009.

- the numbers of workers employed was higher in 2012 than in 2010.

- the amount produced per worker rose fastest between 2011 and 2012.

ANSWER- OPTION (D)

Labor productivity= Total output/total labor. Labor productivity measures the amount of goods and services produced by a worker per unit of time. Labor productivity is a measure of a country’s output efficiency. According to the table, the output worker rose from 100 to 102 between 2010-2011. It rose the fastest from 102 to 111 between 2011 and 2012. Higher labor productivity does not necessarily imply higher output. It may also imply that the same output is being maintained while reducing the level of inputs (labor).

Q.8. The table below shows values of income elasticities of demand for four goods,W, X, Y and Z

| Good | Estimate of income elasticity of demand |

|---|---|

| W | +0.52 |

| X | +0.61 |

| Y | −0.49 |

| Z | −0.57 |

From the table, it may be concluded that

- the demand for all four goods is price inelastic.

- the cross price elasticity of demand between Good X and Good W is positive.

- as incomes rise, the demand for Good Y and Good Z will rise, but by a smaller percentage.

- as incomes fall, only the demand for Good Y and Good Z will rise.

ANSWER – OPTION (D)

As income fall, only the demand for good Y and Z will rise.

Income elasticity of demand refers to the responsiveness of the quantity demanded of a good or service to a change in the income of the people.

Negative income elasticity of demand means that an increase in the income of the people will result in the fall in the demand of the good as they switch to better substitutes.

Positive income elasticity of demand means that an increase in the income of the people will lead to a rise in the demand of the good. Here, good W and X have positive income elasticity of demand which means that a fall in income will result in a fall in demand of the goods W and X. on the other hand goods Y and Z have negative income elasticities which means that when income falls, the demand for these goods will rise.

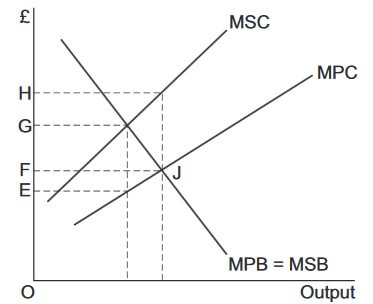

Q.9. The diagram below shows the marginal private benefit (MPB) and marginal social benefit (MSB) curves and the marginal private cost (MPC) and marginal social cost (MSC) curves for Good X produced by a firm. The free market equilibrium position is at point J.

Which one of the following government policies should be used to correct the market failure that exists at point J?

- A per unit subsidy of FH

- A per unit tax of FG

- A per unit subsidy of EG

- A per unit tax of EG

ANSWER – OPTION (D)

From the diagram, we can clearly infer that we have a case of negative externality where marginal private cost (cost to the producer due to employment of additional input) is less than the marginal social cost (the cost to the society for every additional unit produced by the producer) leading to a deadweight loss of EJH. Thus per unit tax of EG must be charged from the producer to make them pay the full social cost of the good. The per unit tax increases the marginal private cost. The tax is charged for every unit until MPC=MSC.

Q.10. In February 2011, British Gas announced record profits for the second year in a row from supplying gas to UK households. Just months after these record profits, British Gas announced price rises of 18%. The increase in price makes it more likely that British Gas has been exploiting its monopoly power.

From the data given, which one of the following is most likely to be correct?

- The 18% price rise is an example of a barrier to entry into the market.

- British Gas is efficient because it made record profits in the two years leading up to February 2011.

- The gas supplied by British Gas has positive externalities in consumption.

- There is a high degree of concentration in the UK market for gas supplied to households.

ANSWER – OPTION (D)

There is high degree of concentration in the UK market for gas supplied to households.

Market concentration refers to the extent to which sales in a market are dominated by one or two business. High degree of market concentration leads to a monopolistic or oligopolistic market structure.

Increase in prices by 18% makes it clear that the British gas is exploiting its monopoly powers. British gas enjoys high amount of market concentration which makes it a price setter in the UK gas market.

Q.11. A pure public good is always

- provided by the government for all consumers.

- provided free of charge because there is no opportunity cost.

- available for consumption by others when consumed by an additional person.

- heavily subsidised by the government.

ANSWER – OPTION (C)

A pure public good is always available for consumption by others when consumed by an additional person.

A public good is a non- excludable and a non-rivalrous good.

In economics, a good or a service is non-excludable when it is not possible to prevent people who have not paid for it from having access to it. A good or service is non-rivalrous if its consumption by one consumer do not prevent simultaneous consumption by any other consumer.

Q.12. The natural environment in the UK is under threat from urbanisation as more and more new houses are built on unspoilt countryside. It has been estimated that by 2050 a fifth of England could be urbanised.

From the passage above, it can be inferred that

- the natural environment is an economic resource.

- the opportunity cost of land is zero.

- the price of land for house building is lower than the price of land for farming.

- the private cost of urbanisation is greater than its social cost.

ANSWER – OPTION (A)

A natural environment of a country is its economic resource.

Natural resource economics focuses on the demand, supply, and allocation of the earth’s scarce natural resources efficiently.

Natural resources are important economic assets. A country rich in natural resources enjoy easy availability of natural raw materials required in the production of various goods having great economic value.

Q.13. Which one of the following combinations, A, B, C or D, is true for a normal good which has a downward sloping demand curve?

| Income elasticity of demand | Price elasticity of demand | |

|---|---|---|

| A | Positive | Positive |

| B | Positive | Negative |

| C | Negative | Negative |

| D | Negative | Positive |

ANSWER – OPTION (B)

Normal goods have positive income elasticity of demand and negative price elasticity of demand.

In economics, normal goods refer to those goods, the demand for which rises with rise in income and falls with fall in the income of the consumer (assuming price remains constant). In other words, normal goods have positive income elasticity of demand.

Price elasticity of demand refers to the responsiveness of quantity demanded to changes in the price of the good, ceteris paribus.

Price elasticities are always negative, confirming to the law of demand, except for giffen goods. Negative price elasticities mean that the demand of a good falls when the price of that good rises and demand rise when the price fall.

Q.14. A government subsidy would cause the largest fall in the price of a product if its price elasticity of demand (defined as a positive number) were

- less than 1.

- 1.

- greater than 1.

- infinity.

ANSWER – OPTION (A)

A government subsidy would cause largest fall in the price of a product if the price elasticity of that product is less than 1.

When the price elasticity is less than 1, then a fall in the price increases the demand less proportionately. So in order to increase consumer demand by larger amount, the government will have to decrease the prices by larger amount. This means the government will have to provide large amount of subsidy.

Q.15. The diagram below shows the market for Good X.

Which one of the following would cause a rightward shift of the supply curve from S1 to S2?

- An increase in the demand for Good X

- The creation of a monopoly by the firms in the industry supplying Good X

- A reduction in the rate of Value Added Tax (VAT) applied to Good X

- A decrease in the cost of the raw materials used in the production of a substitute good

ANSWER – OPTION (C)

The reduction in value added tax (VAT) on good x will shift the supply of the good X rightwards.

Value added tax raises the input costs faced by the producers. So, when the VAT charged decreases, the input cost faced by the producer thus leading to increased supply. For the demand remaining unchanged, higher supply lowers the price of the Good X. the producer passes on the benefit of lower input costs to the consumers in the form of low VAT by reducing the prices.

Q.16. Which one of the following is associated with a missing market?

- A monopoly restricting output

- The production of a negative externality

- A firm deciding to produce a private good

- A government subsidising agricultural production

ANSWER – OPTION (B)

Negative externality refers to the cost suffered by a third party as a result of an economic transactions. The most important feature of any externality, be it positive or negative, is that they do not have markets. Example: A firm produces a product and dumbs the waste into the river (causing water pollution) which affects many fisheries located down the river stream. This is a case of negative production externality where pollution is a good which is a concern for the fisheries. However, there is no market for the pollution. This lack of market for externalities lead to many serious problems when there are no defined property rights.

Q.17. A market is defined as being in equilibrium when

- there is maximum output at minimum cost.

- prices are at their lowest possible level.

- there is no tendency for the market price to change.

- consumer satisfaction is maximised.

ANSWER – OPTION (C)

A market is defined to be in equilibrium when there is no tendency for the market price to change.

Market equilibrium occurs when quantity demanded equals supply. At market equilibrium, price is such that the market clears.

When quantity Demanded>quantity supplied: In this situation market price is below the equilibrium price. There is shortage of Good X in the economy which will drive prices up due to competition among consumers to buy the limited quantities of the Good X. This will continue until the price reaches equilibrium level (P) again. Thus, market will again reach equilibrium point (E) where demand=supply.

When quantity Supplied >quantity demanded: In this situation, the market price is above the equilibrium price (P). The market is in surplus for Good X which will result in fall in prices due to competition among sellers to sell their produce. This process will continue until the equilibrium level of quantity and price (at Q and P respectively) is achieved.

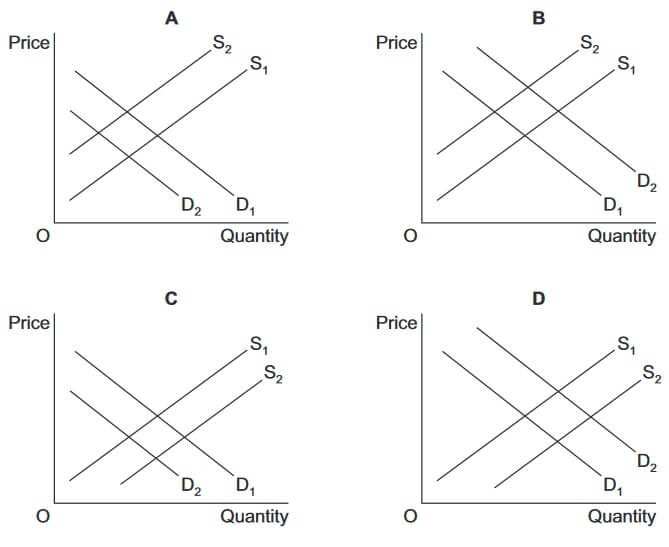

Q.18. In the diagrams below, S1 and D1 show the original supply and demand curves for Good X, while S2 and D2 show shifts of these curves.

Which diagram, A, B, C or D, illustrates the effects of an increase in the price of a good that is complementary to Good X and an increase in labour productivity in the production of Good X?

ANSWER – OPTION (C)

Complementary goods refer to those goods which have to be consumed together in order to satisfy a single want. Example: car and petrol.

An increase in the price of a complementary good (say, petrol) will reduce the demand for Good X (car) as increase in the complementary good (petrol) makes it expensive for the consumer to buy good X (car) as both have to be consumed together. As a result, the demand curve shifts leftwards from D1 to D2.

Now an increase in labor productivity means that there is increase in the efficiency of the labor in terms of output produced per unit of time. This leads to shift in the supply curve towards right from S1 to S2.

Q.19. The price elasticity of demand for a good made by a firm is −0.6. If the firm raises the price of the good, its revenues will

- rise.

- stay the same.

- fall by more than 6 per cent.

- fall by less than 6 per cent.

ANSWER – OPTION (A)

The price elasticity of -0.6 imply that if price of a good increases by 1% then the quantity demanded for that good will fall only by 0.6%. this means that increase in price reduces the demand by relatively less proportions.

Revenue = (Price)*(quantity)

Now, as the price increases then the quantity reduces by les proportions which makes it clear that the revenue of the firm rises.

Q.20. Specialisation and the division of labour require

- firms to be productively efficient.

- the economy to be on its production possibility boundary.

- a means of exchanging goods and services.

- competitive markets.

ANSWER – OPTION (C)

In economics, specialization refers to a situation where individuals and firms, regions and nations (who are willing to trade with other nations) concentrate upon producing some goods and services rather than others.

Division of labor refers to the separation of tasks in an economic system so that the participants can specialize.

Specialization and division of labor requires a means of exchange of goods and services. For example: countries that do not produce a particular good X can acquire it from other nation through trade. Rather than producing Good X, it can concentrate or say specialize in the production of any other good which they can produce efficiently. This will help in dealing with the problem of scarcity in individual countries.

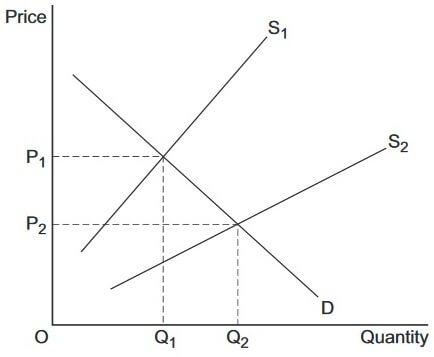

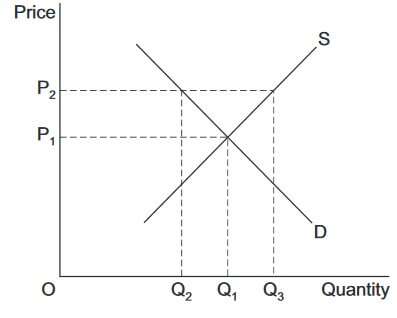

Q.21. The diagram below shows the demand and supply curves for sugar in an economy.

The free market price of sugar is OP1. The government has decided to maintain a price of OP2 and to do so through intervention buying. In achieving a price of OP2, the amount spent on intervention buying by the government would be

- OP1 x OQ1

- OP2 x OQ2

- OP2 x Q2Q3

- OP2 x OQ3

ANSWER – OPTION (C)

OP2× Q2Q3

Here, the government has set the minimum price of sugar at OP2. This is a case of binding price floor. At price OP2 (which is above the equilibrium price OP1), there is excess supply of sugar in the economy by the amount Q2Q3. Now the government indulges in intervention buying where it buys all the surplus amount Q2Q3 in order to achieve the price level OP2.

Thus, the amount that will be spent on intervention buying is OP2× Q2Q3.

Q.22. Public goods result in market failure because

- in the absence of government intervention, a working market for the product is unlikely to become established.

- pure public goods are both rival and excludable.

- the positive externalities in consumption exceed the private benefits.

- the marginal social cost of providing public goods exceeds the marginal social benefit.

ANSWER – OPTION (A)

Public goods result in market failure because in the absence of government intervention, a working market for the product is unlikely to become established.

Public goods are non-excludable and non-rivalrous.

In economics, a good or a service is non-excludable when it is not possible to prevent people who have not paid for it from having access to it. A good or service is non-rivalrous if its consumption by one consumer do not prevent simultaneous consumption by any other consumer.

A good has a market because firms want to sell that good in order to make profit. However, as public goods are non-excludable and non-rivalrous, the marginal cost (MC) of the public good is $0 which means the firm has to set the price equal to $0 (assuming perfect competition, where efficient allocation of goods take place when P=MC). Thusin absence of government, free market forces would fail to provide the good as no one will sell a good free of cost.

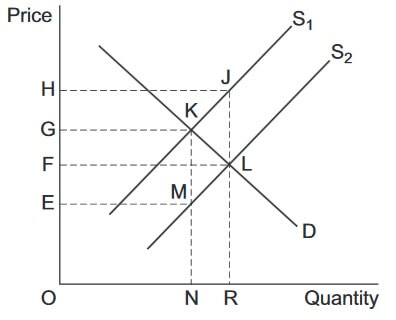

Q.23. In the diagram below, the government grants a subsidy to manufacturers of loft insulation. This shifts the market supply curve from S1 to S2.

The total amount spent by the government on subsidies is represented by the area

- OHJR.

- FHJL.

- OFLR.

- EGKM.

ANSWER – OPTION (B)

The government subsidy leads to a rightward shift in the supply curve from S1 to S2 leading to lower equilibrium price (F). The amount of subsidy is shown by vertical distance JL. Thus, amount spent by the government on the subsidy, to reduce the equilibrium level of price to F, is FHJL.

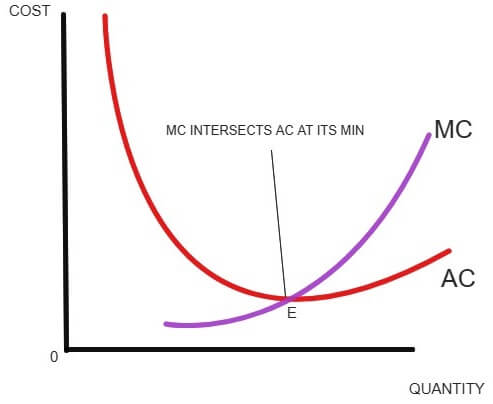

Q. 24. A firm is productively inefficient if

- it can lower its average cost of production by reducing its output.

- an increase or a decrease in output will lead to a rise in its average cost of production.

- it can increase labour productivity by increasing the amount of capital it employs.

- the price it has to pay for raw materials and components is increasing.

ANSWER – OPTION (A)

The MC curve always intersect the AC at the minimum. When the marginal cost is greater than the average cost, MC pulls the average cost up which is shown as a rising AC. When MC is the less than the AC, MC pulls the AC down which is shown as a falling AC. Now when MC is equal to AC, then AC does not change and hence it is at its minimum.

Thus, a firm will produce efficiently till its marginal cost (MC) is equal to the average cost (AC). So, if a firm is able to reduce cost by producing additional unit, then it is profitable to produce more until MC=AC. If further production takes place, then average cost will increase.

Q. 25. All other things being equal, in a monopoly

- market power always leads to an efficient allocation of resources.

- product differentiation leads to low barriers to entry.

- economies of scale lead to a downward sloping market demand curve.

- high prices can lead to market failure.

ANSWER – OPTION (D)

Market failure occurs when there is under provision of a particular good i.e. there is no efficient allocation of goods and services. A monopoly always leads to the creation of deadweight loss to the economy.

Higher prices charged by the monopolist cause the deadweight loss to increase as more people are unwilling to buy the good which they would have if the economy was operating under perfect competition (where, P=MC). The monopolist produces where marginal revenue is equal to marginal cost (MR=MC). The price is determined by the demand curve at this quantity. Unlike perfect competition, the monopolist charges price such that MC. Thus, there is underproduction in the economy by the monopolist (as price charged by the monopolist is higher than what is charged in perfect competition) leading to market failure.

Section B: Data Response

Context 1

MARKETS: DO THEY BENEFIT ALL?

Assignment Extracts A, B and C, and then answer all parts of Context 1 which follow.

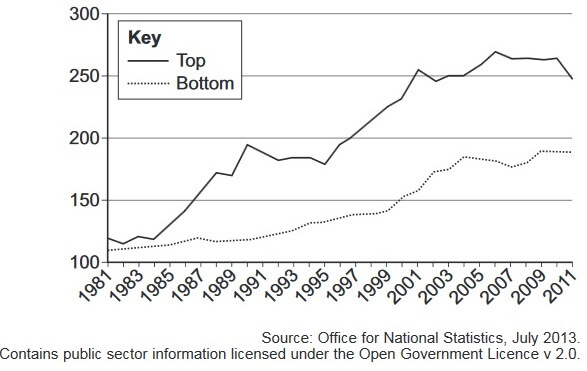

Extract A: Index of real household disposable income of two income groups*, 1981 to 2011, 1977 = 100

* ‘Top’ refers to the highest earning / 20% of households; ‘Bottom’ refers to the lowest earning / 20% of households

Extract B: Markets at work

Adam Smith, the eighteenth century economist, wrote of the ‘invisible hand of the market’. He believed that, left to its own devices, a market would ensure that resources are allocated to their best uses for the benefit of all. Changes in prices would coordinate the decisions between consumers and producers. Indeed, it is largely as a result of the market mechanism that 63 million people in the UK are fed and clothed every day. How could a government hope to plan for such an undertaking? For instance, consumers can buy fresh food or processed food; they may eat in, eat out or on the go; they can dress in designer wear, sportswear or work wear. The list is endless.

However, buying decisions can be influenced by powerful producers. Indeed, the power of brand names such as iPad and Coca-Cola can be a significant barrier to entry. It can reduce competition in markets and lead to some firms possessing monopoly power. Consequently, consumers may face reduced choice and may have to pay higher prices to obtain what they perceive to be the best product. Moreover, in reality, advertising also plays a key role in the allocation of resources. Its influence, in some markets, has been criticised, and there have been calls for greater regulation. Advertising can encourage increased consumption of goods and other activities which give rise to negative externalities, such as gambling. In some cases, this has led to financial ruin, family breakdown and health problems; yet the total number of gambling advertisement slots on UK television increased from 152 000 in 2006 to 1.39 million in 2012. Statistics show that those in the lowest income group spend, on average, more per week on gambling than they do on taking part in sports activities.

Extract C: Do markets work ethically?

Can consumers always buy what they really need? One of the main determinants of a consumer’s demand is income. Whilst income inequality has reduced slightly over the past few years, in 2011/12 the highest earning fifth of UK households had an average income of £78 300, compared with £5400 for the lowest earning fifth – a ratio of 14.5 to 1. Those with higher incomes have more spending power, which inevitably leads to higher prices in certain markets, excluding those who earn less. In 2011, for example, 9% of the population felt that they were unable to afford their mortgage or rent payments, whilst 30% felt that they were unable to afford a week’s annual holiday.

One problem with markets is that there is no consideration of ethical issues. Resources are allocated on the basis of demand backed by willingness and ability to pay, and not necessarily with the general well-being of society in mind. For those people who earn very low incomes, and for those who are unemployed, life can be a struggle. As the political economist, Will Hutton, wrote recently: ‘At the bottom, a world of food banks, payday lending and quiet desperation. And at the top, an extravagantly-paid elite.’ So do markets work well, as Adam Smith suggested, or do they lead to market failures such as those arising from income inequalities, monopolies and negative externalities?

Q.1. Define the term ‘income inequality’

ANSWER

Income refers to the flow of cash or cash equivalents received in the form of wage or salary, rent, interest or profit.

Income inequality refers to the extent to which the earnings or money is unevenly distributed among the various participants of an economy. The income inequality arises when the benefits of economic growth in the form of higher income is not shared fairly.

The rising gap between the rich and the poor leads to immobility of income as well as a lack of opportunities available, reflecting continuous disadvantage for a particular section of the society (the poor). Widening inequality can severely affect the growth and macroeconomic stability of a country and lead to concentration of powers in few hands.

Q.2. Using Extract A, identify two significant points of comparison between the changes in real household disposable income for the two income groups over the period shown.

ANSWER

The two significant points of comparison between the changes in the real disposable income for the two income groups (highest earners and lowest earners) over the period shown (1981-2011) are as follows:

a) There was growth in real disposable income for both the groups over the period shown (1981-2011). The highest earning group grew from an index of 115 (approx) in 1981 to an index of 240 (approx) in 2011.

On the other hand, the real disposable income of the bottom or lowest earning group grew from an index of 110 (approx) in 1981 to an index of 190 (approx) in 2011.

b) The top income group enjoyed the most rapid growth in the real disposable income between the period 1981 and 2011. Their real disposable income grew by 108.69% {(240-115)/115} or by an index of 125 over the period shown. The lowest income group however recorded a real disposable income growth of 72.7% {(190-110)/110} or by 80 on index over the period shown.

Q.3. Extract B states that: ‘Changes in prices would coordinate the decisions between consumers and producers.’ Explain how changes in prices allocate scarce resources in a market economy.

Now in the long run, as firms realize that due to rationing of some consumers, their profit is diminishing. Thus they will no longer have any incentive to supply goods to the market and thus will leave the market to reallocate their scarce resources in other market having scope of profits.

This is how the price, through its 3 functions, facilitates efficient allocation of scarce resources.

ANSWER

In economics, Price mechanism is the manner in which prices of goods or services affect the supply and demand of goods and services. The price mechanism has three functions:

- Signaling: When price of a good changes, it sends signal or provides information to firms and consumers. When price rises, then this give signal to consumers to reduce the quantity they demand or withdraw from the market. Higher prices give signal to producers to enter the market and supply more quantities.

Similarly, lower prices provide signal to consumers to increase their demand or encourages potential buyers to enter the market. Lower prices, however, signal producers to leave the market.

- Rationing: When a particular good becomes scarce, then the demand for that good exceeds its supply. This drives up the price of that good. As a result of increase in price. Some consumers who cannot afford to buy the good are rationed out of the market.

- Incentive: Higher prices provide an incentive to existing producers to supply more as they expect higher profits. This also serves as an incentive for new producers to join the market. This leads to increase in the supply of the good in the market.

Q.4. Extract C states that: ‘One problem with markets is that there is no consideration of ethical issues.’ Using the data and your knowledge of economics, evaluate the view that governments should intervene to correct market failures such as those arising from income inequality, monopolies and negative externalities.

ANSWER

Market failure refers to a situation in which allocation of resources through price mechanism is not efficient. Market failure includes externalities, information asymmetries, factor immobility, public goods which are both non-excludable and non-rivalrous, monopoly power which results in high prices of goods etc.

Income inequality refers to the extent to which the earnings or money is unevenly distributed among the various participants of an economy. The income inequality arises when the benefits of economic growth in the form of higher income is not shared fairly (equitably).

In a free market economy, government considers that the markets are the best way to allocate scarce resources and allow the market forces of demand and supply to set prices and the role of the government is limited to the protection of the property rights, maintaining the currency value and the law & order in the country. Government usually intervene in the market system when:

- The market fails to allocate resources efficiently.

- The market fails to distribute the income and wealth equitably.

- To introduce policies that improve the performance of the economy and bring it out of prolonged recessions.

A monopoly always leads to the creation of deadweight loss to the economy.

Higher prices charged by the monopolist causes the deadweight loss to increase as more people are unwilling to buy the good which they would have if the economy was operating under perfect competition (where, P=MC). The monopolist produces where marginal revenue is equal to marginal cost (MR=MC). The price is determined by the demand curve at this quantity. Unlike perfect competition, the monopolist charges price such that P>MC. Thus, there is underproduction in the economy by the monopolist (as price charged by the monopolist is higher than what is charged in perfect competition) leading to market failure.

Negative externality refers to an economic activity that negatively affects a third party which is not part of that activity. This type of externality can arise either during the production or consumption of goods and services. For example: A factory near residential area causing noise pollution is a case of negative externality (noise pollution is the negative externality).

The market is governed by price mechanism where prices decide the demand and supply. The market does not know what is meant by equitable distribution. As mentioned in the extract C, resources are allocated in a market economy on the basis of demand backed by willingness and ability to pay and not necessarily with the general well-being of the society in mind. Thus, it is said that market does not considers the ethical issues i.e. it has no cognizance of right or wrong.

Thus, as mentioned earlier, the government intervention is required and is inevitable in the cases when market fails to allocate resources equitably, and remove negative externalities.

Context 2

GOVERNMENT SUBSIDIES: TO GIVE OR NOT TO GIVE?

Assignment Extracts D, E and F, and then answer all parts of Context 2 which follow.

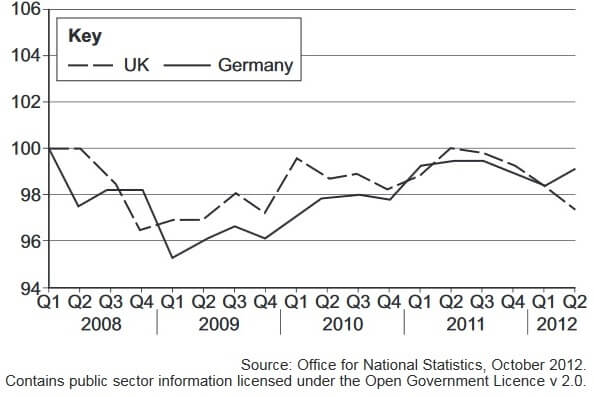

Extract D: Index of UK and Germany labour productivity, output per hour, Q1 2008 = 100

Extract E: A benchmark for UK productivity?

In 2013, the UK Government gave a subsidy of £9.3m to the Japanese car firm, Nissan, as an incentive for it to produce a new model of car at its factory in Sunderland. As a result, the Sunderland plant is currently the flagship of UK manufacturing. It employs over 7000 people directly, not to mention the additional 25 000 employed in related markets. The firm operates two assembly lines; it has benefited extensively from specialisation and technical economies of scale. Its workforce is highly trained and labour productivity has constantly improved. The plant recently became the first in the UK to make over one million cars in two years.

Back in the 1980s, Nissan was given financial incentives to open a plant in Sunderland to help reduce the unemployment caused by the decline in industries such as shipbuilding. The situation had been made worse by the market failures of geographical and occupational immobility. But should the firm still receive support? In November, Nissan reported that it expected to make a net profit of 334 billion yen (£2.2bn) for the year ended March 2014.

The Government has also announced that it is prepared to support financially the development of the proposed £16bn nuclear power station in Somerset, in the south west of England, due to be built by the French firm, EDF, with help from Chinese investors. Given the increasingly rapid depletion of non-renewable fossil fuels, some would argue that it is sensible to support the production of alternative energy sources. Yet the impact on the environment in Somerset must also be considered.

Extract F: What, how, for whom – who is more deserving?

Government support is not provided to all firms. For instance, the DVD and games rental firm, Blockbuster, and the music and film retailer, HMV, have, arguably, suffered as a result of new technology and structural change. Whilst HMV is still trading, just over 800 jobs were lost at Blockbuster when the firm closed its remaining stores. Nowadays, many consumers find downloading more convenient, and further advances in technology have led to the streaming of music and films. The online TV and film streaming firm, Netflix, reported a huge increase in demand for its services; it ended 2013 with 44 million international viewers. The power of the consumer reigns and, as a consequence, the ‘old’ industry is left behind.

But is this fair? How does a government decide which firms to support financially? There are those who argue that firms should be left to fend for themselves, that government subsidies should be used only for goods and services whose production and consumption give rise to positive externalities.

A defibrillator, for example, a life-saving machine for use when a person’s heart stops, could be described as a merit good. According to the charity, The British Heart Foundation, there are around 60 000 out-of-hospital cardiac arrests (heart failures) in the UK every year, yet the provision of defibrillators is not routinely subsidised by the Government. More and more community organisations are holding fund-raising activities to enable them to acquire their own defibrillators, but should they have to? Is this the best way to maximise economic welfare?

Q.5. Define the term ‘technical economies of scale’ (Extract E).

ANSWER

Technical economies of scale: Economies of scale refers to reduction in the average cost of production as the scale of production expands. Technical economies are achieved when there is increase in the efficiency of production process. The lower or decreasing average total cost represents improvement in the productive efficiency of the firm.

Internal economies of scale refer to the economies in production which a firm achieves itself when it expands its output. Technical economies of scale are an internal economies of scale wherein large firms are able to take its advantage by introducing efficient techniques of production and thus indulging in large scale production.

Example: A large plant is always cheaper to run as it requires less staff, less energy and most importantly it increases the level of production with low overall cost of production.

Q.6. Using Extract D, identify two significant points of comparison between changes in labour productivity in the UK and Germany over the period shown.

ANSWER

Following are the two points of comparison between the labor productivity (output per hour) in the UK and Germany over the period shown (2008-2012):

a) Lowest & highest labor productivity index: Labor productivity index in Germany was lowest in the 1stquarter of 2009, at an index of 95 (approx.) while the index of labor productivity in Germany was highest in 1st quarter of 2008 (start of the period), at an index value of 100.

Labor productivity in the UK was the lowest during the 4th quarter of 2008 at an index value of 96.7 (approx.). The labor productivity was highest in the UK in 1st & 2nd quarter of 2008 or at the 2nd quarter of 2011 at an index value of 100.

b) Labor productivity index for both UK and Germany started from an index value of 100. However, in the 2nd quarter of 2012, labor productivity of Germany ended with an index value of 99 (approx.), while labor productivity of the UK ended much lower with an index value of 97 (approx.).

Q.7. Extract E states that: ‘The firm operates two assembly lines; it has benefited extensively from specialisation and technical economies of scale ... .’ Explain how specialisation may lead to increases in productivity and competitiveness.

ANSWER

Specialization refers to concentrating on and becoming expert in a particular area of skill. When labor specialization takes place, it is known as division of labor. Division of labor refers to a process where each task is assigned to a specific worker by breaking the job into discrete tasks. When a specific task is performed by a specific worker, he is more likely to become highly skilled because of repetition of the assigned task and will be able to achieve the goal more quickly and efficiently.

The productivity of each worker rises as there is efficiency in allocation. Each worker is assigned a task which makes entire use of his/her skill, making the production cost effective.

The labor specialization also leads to minimum wastage of time in transitioning between the tasks as each worker always performs a specific assigned task. For example: Consider a car manufacturing factory where each worker is assigned a specific task such that car painting and assembling is done by two different workers. Now when a worker finishes painting a car, he does not have to waste the time in picking up required tools to assemble the car as that is being done by another worker.

When productivity increases, then the firm is able to produce more units of output in the same amount of time period leading to fall in the average total cost of production. Productivity increase also helps the firm to lower its prices in comparison to its competitors while providing higher quality of goods and services. This increases the competitiveness of the firm in the market. The firm enjoys higher market share.

Q.8. Extract F states that: ‘There are those who argue that firms should be left to fend for themselves ... .’ Using the data and your knowledge of economics, evaluate the view that firms in industries such as cars and energy should operate without any financial assistance from governments.

ANSWER

Market mechanism (or price mechanism) shows how the limited resources are allocated in the economy through the determination of prices by the forces of demand and supply. The price mechanism helps in determining the way in which the resources are allocated through rationing of consumers, and by providing incentives to producers to enter or exit the market in order to relocate the resources. Thus, market forces, without any government intervention, is able to allocate the resources in the economy efficiently.

In a free market economy, government considers that the markets are the best way to allocate scarce resources and allow the market forces of demand and supply to set prices and the role of the government is limited to the protection of the property rights, maintaining the currency value and the law & order in the country. Government usually intervene in the market system when:

- The market fails to allocate resources efficiently.

- The market fails to distribute the income and wealth equitably.

- To introduce policies that improve the performance of the economy and bring it out of prolonged recessions.

Market failure refers to a situation in which allocation of resources through price mechanism is not efficient. Market failure includes externalities, information asymmetries, factor immobility, public goods which are both non-excludable and non-rivalrous, monopoly power which results in high prices of goods etc.

The car industry globally generates large amount of employment opportunities. It is currently a major driving force for many significant industries like steel, iron, aluminum, plastic, glass, electronics, insurance, transport and many more throughout the world.

Energy industry is a pivotal part of the infrastructure and maintenance of society in every economy. Economic growth significantly influences energy consumption. This is because as an economy develop and living standards of people improve, energy demand also grows rapidly. In the present world, increasing concerns of fossil fuels emissions on the environment is encouraging the world to shift to non-fossil renewable sources of energy.

There is enough evidence from the given extracts, for the government to provide financial assistance to the car and energy industry. Government is required to financially incentivize the car manufacturing companies to open their plants in structurally backward regions as they are worse hit by factor immobility causing structural unemployment. The government can provide financial assistances to the car manufacturers in the form of subsidies.

The energy industry should also receive financial assistance from the government to support the production of alternative energy sources, given the rapid depletion of non-renewable fossil fuels.

However, the financial support by the government should not be given indefinitely. As is clear from the Extract E that Nissan, which got financial incentive from the government in 1980s, to open a plant in Sunderland expected a net profit of 334 billion yen by the year ended march 2014.

Thus, the government should provide incentives only when there is market failure, i.e. the market is not able to produce efficient results on its own. In all other cases, the firms should be left to fend for themselves. The government support is not required by all the firms. As mentioned in Extract F, Government subsidies and other incentives must be used for only goods and services whose production and consumption give rise to positive externalities.